When people hear the term “401(k) millionaire,” they often assume it takes special investment skill or unusually high income.

The truth is far simpler. According to Fidelity, more than 650,000 Americans now have over $1 million in their 401(k) accounts alone—a record high. Most of them aren’t professional investors. They’re regular employees who followed a few basic rules for a long time.

This first article in our retirement series explains how they did it—and why the answer has more to do with time and compounding than talent.

Who Are 401(k) Millionaires?

The average 401(k) millionaire is about 59 years old and has been contributing for 25 years or more. They didn’t rely on complex strategies or lucky stock picks. Instead, they steadily invested through market ups and downs and allowed compounding to work in the background. Their success wasn’t dramatic—but it was powerful.

The Most Important Factor: When You Start

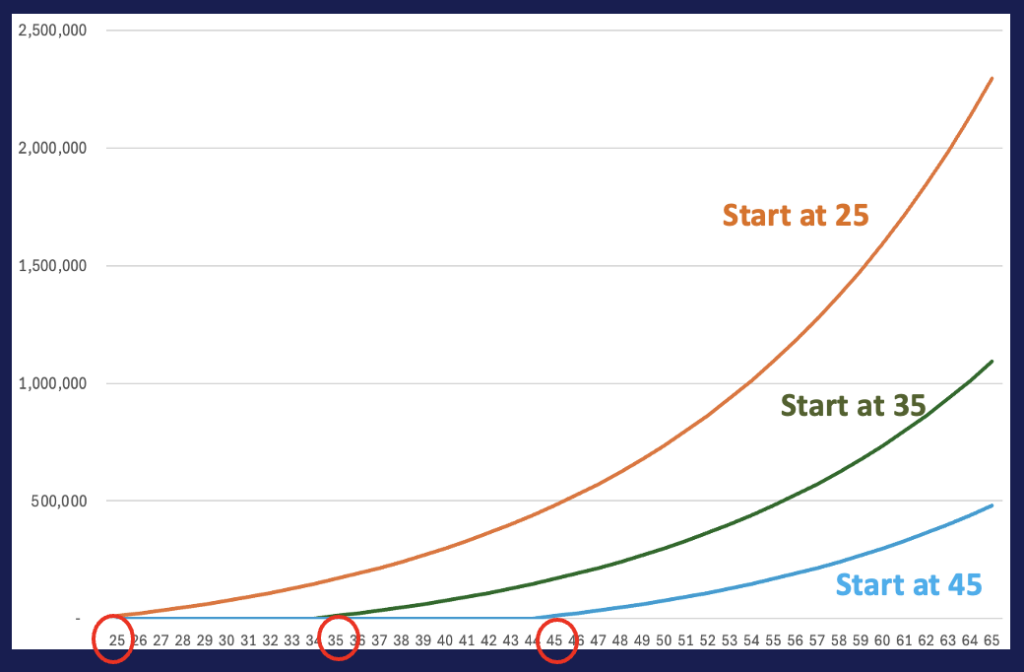

Time matters more than contribution size. Imagine three people who each invest $10,000 per year, earning 7% long-term returns:

One starts at 25, One starts at 35, and One starts at 45

By age 65:

– The 25-year-old starter ends with over $2 million

– The 35-year-old reaches about $1 million

– The 45-year-old has roughly half of that

Same annual investment. Very different outcomes.

In retirement investing, time is your greatest asset.

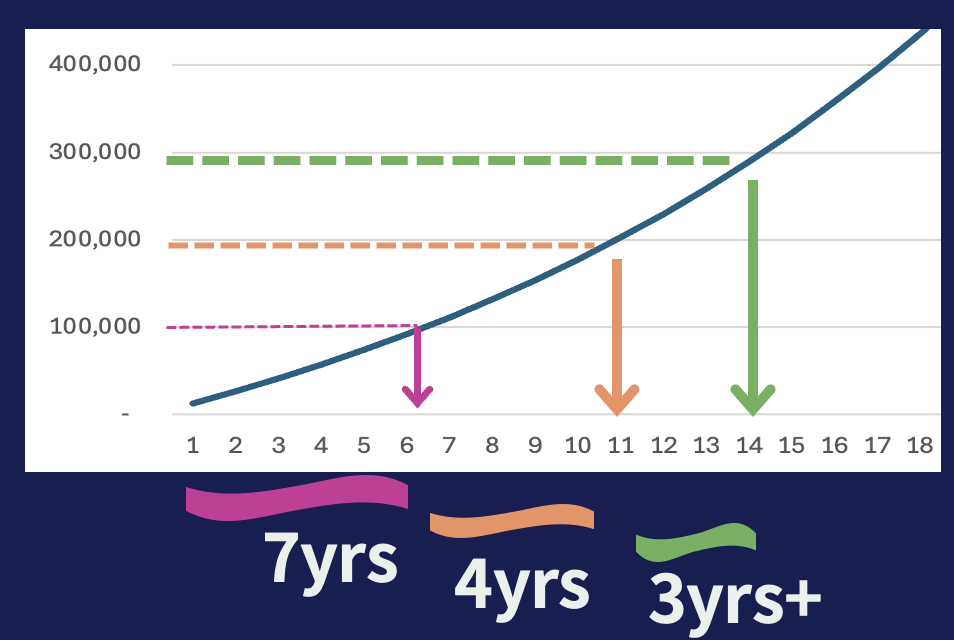

Why Compounding Feels Slow—Until It Doesn’t

Compounding is simple: your gains begin earning gains. Early on, progress feels slow. That’s why many people lose patience. But compounding accelerates later.

For example, investing $1,000 per month at 7%:

– The first $100,000 may take about 7 years

– The next $100,000 takes much less time – 4 years

– Growth speeds up as your balance grows

That’s why many 401(k) millionaires see their biggest gains later in life. Compounding doesn’t shine early—it shines consistently.

What Actually Works

The path most 401(k) millionaires followed is straightforward:

— Start as early as possible

— Contribute every year

— Always take the employer match

— Stay invested through market volatility

Do these things long enough, and the results often look extraordinary—even though the process is not.

What Comes Next in This Series

401(k) millionaires aren’t rare because it’s impossible.

They’re rare because many people start late, stop early, or leave the market during downturns.

That leads to the next big questions:

– What percentage of Americans reach retirement with at least $1 million in savings?

– Do you really need $1 million to retire comfortably?

– What does “comfortable retirement” really cost today?

👉 Part 2 of this series will dig into the data and reveal the real numbers behind retirement readiness in America.